Though crude oil prices edged up last week, the market remains well below VirtualOil’s original $50 strike price, meaning the hypothetical portfolio’s production is shut in in the spot market again. Oversupply continues while China GDP forecasted growth is slowing. Given the market outlook, the VirtualOil board has decided to fold the company and, with a hypothetical capital injection, restructure its portfolio at a lower strike price.

Our fictitious options-based VirtualOil portfolio launched just as the market was feeling the initial impacts of the drastic decline of oil prices. We started trading at $75 and today the market is struggling to maintain $45. That $30 of lost value on notional crude reserves of 10 million barrels/day equates to significant losses.

The decision to restructure is an appropriate reflection of some of the hard decisions many producers have faced in this continued low-price environment. Considering the M&A activity taking place in the oil patch, VirtualOil winding down its original structure and reorganizing at a lower strike price reflects some of the consolidation we see in the industry.

In the year since we ramped up the simulation, VirtualOil has netted about $15 million. Closing out the remainder of our positions, we were able to unwind an additional $35 million in value from the portfolio. We then went back to our virtual investors and raised an additional $150 million to restructure the company at a $25 strike price.

That gives us some $200 million to reinvest in options at a more attractive price point in the current market, and the opportunity for our investors to more readily realize value as the portfolio moves forward. In fact, our new strike price matches the operating costs of some of the more efficient producers in the marketplace.

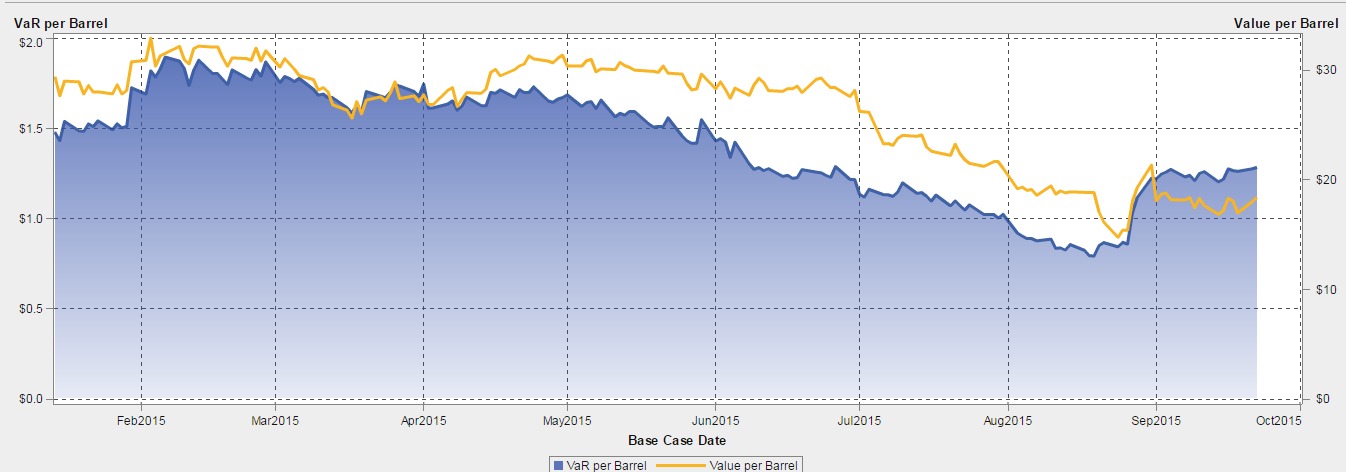

The charts this month represent this restatement of portfolio value and VaR back to January 2015 at $25. You'll notice the associated jump in the value of the rolling portfolio. The second chart shows the restated portfolio with the January start date.

Interestingly, the value at risk (VaR) of our portfolio took a big jump at the end of August as we saw several days of highly volatile prices. The prompt month price jumped from $40 to $50 and has since retreated slowly back down. The jump in prices was due to OPEC discussions about ending the supply surplus as US production finally began to fall.

Assumptions

The hypothetical derivatives-based oil production firm VirtualOil simulates the performance of a generic crude oil asset, and delivers sectorial exposure to the commodity oil market. The reorganized VirtualOil structure starts up with an investment of $200MM in monthly average price call options with a strike price of $25 per barrel on the price of WTI light sweet crude oil. The strip of options starts at 10,000 barrels per day and extends out for 5 years with a 20 percent average annual decline in underlying notional barrels, replicating a physical oil asset. VirtualOil initially holds notional crude oil reserves of approx. 10MM barrels. Monthly cash flow is generated when the daily average West Texas Intermediate (WTI) price relative to the preceding month exceeds $25 per barrel. Cash flow is reinvested monthly at 5 percent and the project winds up when the reserves are depleted.

VirtualOil is managed in SAS® BookRunner with reports surfaced in SAS® Visual Analytics. Click to learn more about SAS® BookRunner’s state-of-the-art Commodity Trading & Risk Management capabilities.

Disclaimer: This is a fictitious portfolio and is not a solicitation to trade.