Year-end outlooks from most analysts project the low-price environment in the oil market will continue for most of next year, but some pundits emphasize that the market has bottomed out and suggest recovery, though gradual, may be seen if increasing demand outpaces supply growth and sops up some of the current excess. But the year is wrapping up with few encouraging signs for the short term.

The price of oil certainly didn’t take much solace from the latest OPEC meeting, dropping under $40 and testing lows not seen in a decade. Rig counts lost another 10, inventories are full, and the prompt month contract is hitting lows not seen since the 2009 post-crash period. Announcements of major reductions in oil firms’ cap-ex for 2016 reflect these realities.

For its part, the most recent Energy Information Administration (EIA) Short-Term Outlook has West Texas Intermediate crude (WTI) prices averaging $49 per barrel in 2016. The forward curve has grown steeper on a relative basis, with the prompt month looking at $35 while prices a year out are $43. That $8 differential gives a clear indication the market expects to see prices increase in the latter part of 2016.

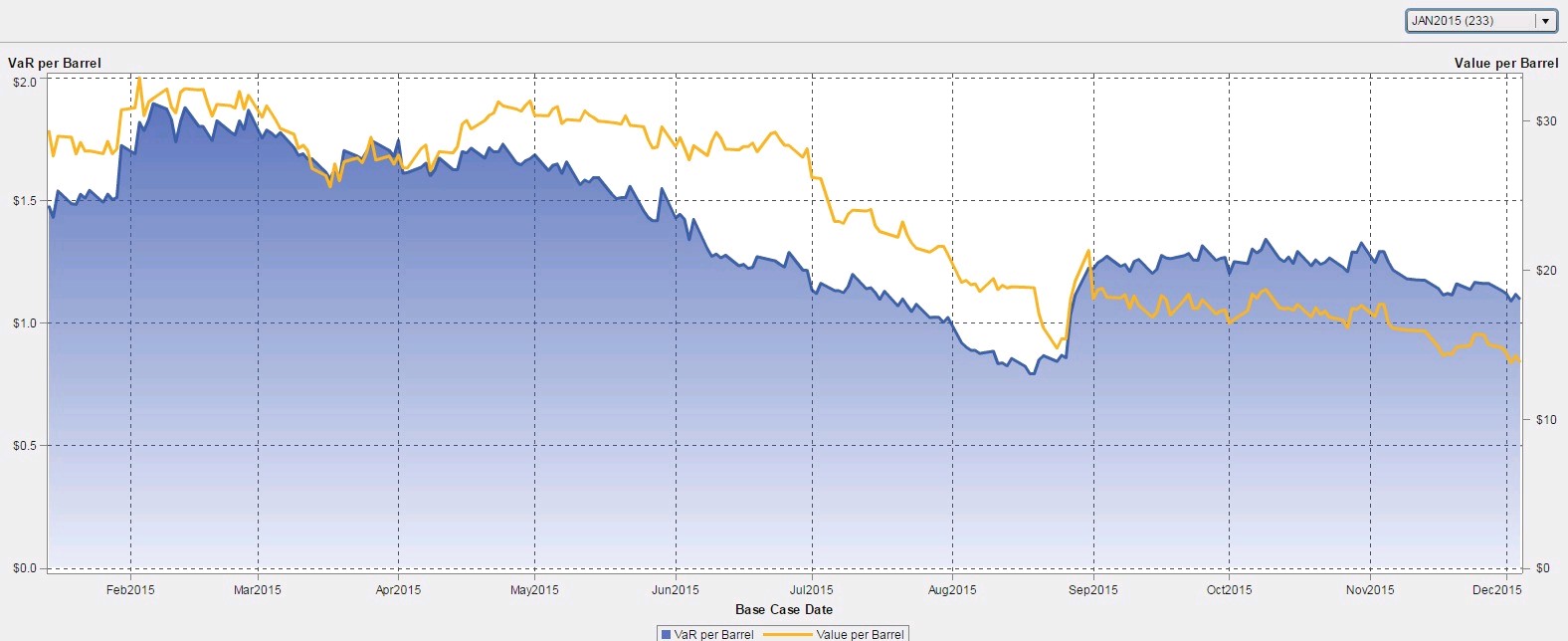

At the front end of the curve, option volatilities are down from 65 percent to 35 percent, impacting the value of the options VirtualOil bases its business on. But the portfolio is still making good money (see chart), largely because our hypothetical, options-based company is not exposed to the layoffs, mergers and bankruptcies facing the physical industry.

Price levels are suppressed on a relative basis across commodities. Whether you look at energies, metals or ags, commodities are looking at 15-year lows. This may suggest a small silver lining, in that commodity prices tend to rise as demand for the real goods that require their input grows. That makes commodities a good hedge against unexpected inflation. Central banks have been holding interest rates and inflation low, but there is much discussion about how much longer it is healthy to do so, particularly now that the US Federal Reserve decided to begin raising the landmark rate this week. The Fed’s move has increased the likelihood of an unexpected rate adjustment elsewhere, a move commodity producers would be hedged against.

Assumptions

The hypothetical derivatives-based oil production firm VirtualOil simulates the performance of a generic crude oil asset, and delivers sectorial exposure to the commodity oil market. The reorganized VirtualOil structure starts up with an investment of $200MM in monthly average price call options with a strike price of $25 per barrel on the price of WTI light sweet crude oil. The strip of options starts at 10,000 barrels per day and extends out for 5 years with a 20 percent average annual decline in underlying notional barrels, replicating a physical oil asset. VirtualOil initially holds notional crude oil reserves of approximately 10MM barrels. Monthly cash flow is generated when the daily average WTI price relative to the preceding month exceeds $25 per barrel. Cash flow is reinvested monthly at 5 percent and the project winds up when the reserves are depleted.

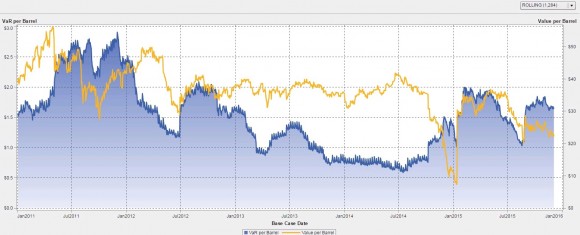

See additional simulations below. VirtualOil is managed in SAS® BookRunner with reports surfaced in SAS® Visual Analytics. Learn more about SAS® BookRunner’s state-of-the-art commodity trading and risk management capabilities.

Disclaimer: This is a fictitious portfolio and is not a solicitation to trade.

VirtualOil VaR Backtesting Dec 2015