Financial institutions are mired with large pools of historic data across multiple line of businesses and systems. However, much of the recent data is being produced externally and is isolated from the decision making and operational banking processes. The limitations of existing banking systems combined with inward-looking and confined data practices makes it tough to make sense of both structured and unstructured data as it arrives.

Simply accessing large amount of data across devices and platforms is challenging, but the story doesn’t end here. A highly connected and online consumer world has changed the once laid-back decision making approach that used to be the forte of branch banking.

To gain customer insights or address risk exposure, decision-making processes must quickly decipher a large volume of internal and external data. This means a nearly heroic task of ensuring that data is accurate, consistent and fit for decision-making purposes within a very short span of time.

Recently I had the opportunity to work with a bank going through a complete transformation of their core banking, cards, risk, data warehouse, financial reporting, CRM and other systems. As the discussions around replacing core banking systems started to heat up, the infamous question of data quality surfaced. It quickly became a foregone conclusion that almost all the major initiatives in the bank hinged upon business and IT settling the score with bad data quality once for all – at least in the short run.

After the initial discussion, the bank quickly realized that most of the critical customer processes around customer on-boarding, know your customer (KYC), single customer view, compliance and risk reporting, CRM, etc., will be gravely affected by the quality of the data.

Without wasting any time we decided to conduct a data quality assessment related to bank’s critical business processes and systems.

Initial Scope

We kept the scope focused on only showing the results of handful of customer data elements. The objective was to trigger a thought process around the importance of data quality and subsequent organizational alignment through the introduction of data governance policies.

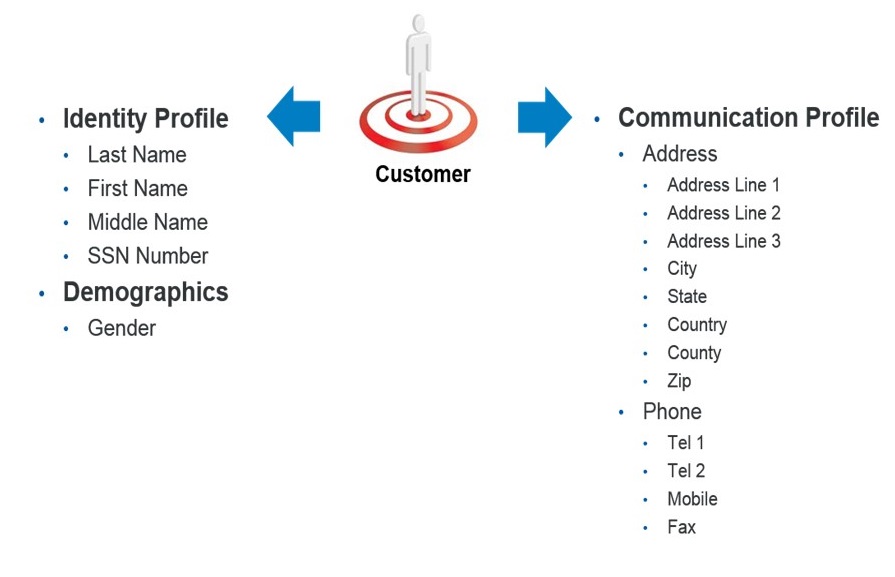

After going through series of Q&A sessions with business users, our list of customer data areas started with profiles around identity, communication and demographics.  This customer information was captured during customer on-boarding/KYC process and subsequently was used to identify data across different sources with aim of sending marketing offers.

This customer information was captured during customer on-boarding/KYC process and subsequently was used to identify data across different sources with aim of sending marketing offers.

What’s next? In my next blog post, I’ll review the process for integrating data quality into the bank’s systems – and the results of that effort.