Traditional artificial intelligence (AI) techniques like machine learning (ML) have been adopted by insurers for some time. This is borne out by the fact that every insurance marketplace maintains some form of regulation speaking to the governance and use of data, models and AI.

More advanced AI technologies, such as generative AI or agentic AI, have yet to prove their true value. But trust in those technologies appears severely imbalanced and detached from reality.

Watch Episode 2 of Brewing Curiosity: Insurance Unfiltered, to learn about creating AI safeguards and different approaches that can be taken to ensure safe model use.

Consider the NAIC Private Passenger Auto Artificial Intelligence / Machine Learning Survey. It showed that nearly 90% of respondents (insurance companies in nine states with at least $75 million in direct written premiums) indicated some use or exploration of AI or ML.

Notably, this survey was:

- Conducted under market conduct examination authority of nine states.

- The data was collected back in 2021.

- The study was published barely a week following the public release of ChatGPT, the “Global AI Zero Hour.”

In an IDC report, commissioned by SAS, we found similar results.

The state of global insurers

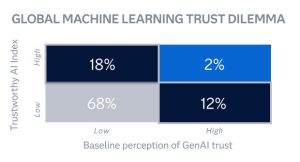

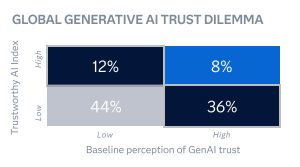

Global insurers responding to the SAS report indicated that about 70% use some form of traditional AI, yet only 7% identify themselves as transformational. In this same report, we found that trust in more advanced AI technologies, like GenAI, eclipses more traditional, deterministic AI capabilities (namely, machine learning) by 200%.

The report also concludes that nearly half (49%) of insurers already use agentic AI – albeit in a limited fashion.

Such truths transcend inconvenience and threaten existential disruption.

There are regulations, such as the EU AI Act, Canada’s Guideline E-23 – Model Risk Management, and Singapore’s Veritas Initiative, that provide frameworks, guidance and yes, penalties for the safe use of AI. But compliance does not represent the clearest and most present danger for insurers.

Survey respondents scoring low on trustworthiness trust GenAI 200% more than traditional machine learning.

AI’s use can cause irreparable and unrecoverable damage to the brand

Your brand is everything. Your brand is anything that anyone thinks when they see your logo or hear your name. Trust takes years to earn, which makes it especially important in this industry. Because AI can annihilate that trust in the blink of an eye.

We look no further than the high-profile class action lawsuit involving Cigna’s PxDx (procedure-to-diagnostic) – an algorithm designed to review preapproved claims, requiring a medical director signoff prior to denial. The troublesome details include 60,000 such claims denied in a single month (at an average of one every 1.2 seconds) – and 80% of denials were overturned on appeal.

The outcomes cannot be debated. Yet abstract principles – such as unfair bias, decision transparency and human-in-the-loop – require experts to help us unpack how the insurance industry can adopt these technologies safely and ultimately add value for customers.

Read how synthetic data can help insurers fill data gaps, improve reliability, and more.Experimentation to implementation

In our series, Brewing Curiosity: Insurance Unfiltered, SAS’ Global Head of Data Science, Dr. Iain Brown, shares why trustworthy decisions made by AI in underwriting, pricing and claims matter so much in his work.

“One of the reasons this topic matters so much in insurance is that your models don’t just predict outcomes; they influence who gets access, at what price, and how quickly someone gets help,” says Brown.

“That means technical performance is necessary, but not sufficient. You need to be able to explain decisions to internal stakeholders, regulators and customers; and you need the ability to detect when a model starts drifting into unfairness as data, behavior and economic conditions change.”

He continues, “From a practical standpoint, I tend to frame the challenge as three layers:

- Data integrity. Are we using the right data, with traceability and quality controls?

- Model integrity. Are we testing for bias, explainability, robustness and stability?

- Decision integrity. Are we applying consistent governance and monitoring once the model is live?

If you get those layers right, you don’t just reduce risk, you build the kind of trust on which insurance depends.”

Brown and I were joined by technology and policy ethics expert, Kristi Boyd. When asked about her observations of the insurance industry’s preparedness to adopt AI and wield it safely, she shared an overall positive view. She notes that insurers already boast strengths in regulatory preparedness and robust governance frameworks. However, they lack capacity and expertise in their workforce.

“Insurers understand risk by definition,” says Boyd. “[They] are used to governance, audit processes, and articulating conversations about fairness and bias. After all, this is a highly regulated industry regardless of your geography.”

“However, insurers are deeply dependent on data,” she continues. “Insurers possess mountains of data. The trick becomes, which data do you choose to use and for what problem? If you choose correctly, you might expect to realize good outcomes. But since so much data is garbage-in/garbage-out, making that choice can prove incredibly problematic, especially at scale.”

“As you scale model use, transparency and explainability become increasingly more complex. You may have heard of the gambler’s fallacy – outcomes that appear correct may seem incorrect to experts, making it difficult to guarantee your decisions (your AI’s decisions) are clear to stakeholders, customers or the general public.”

Trustworthy by design

Today, only about 9% of insurers (1 in 11) fall into what we describe as the “ideal quadrant” for AI use – that is, balancing high trust in the use of AI with trustworthy AI systems.

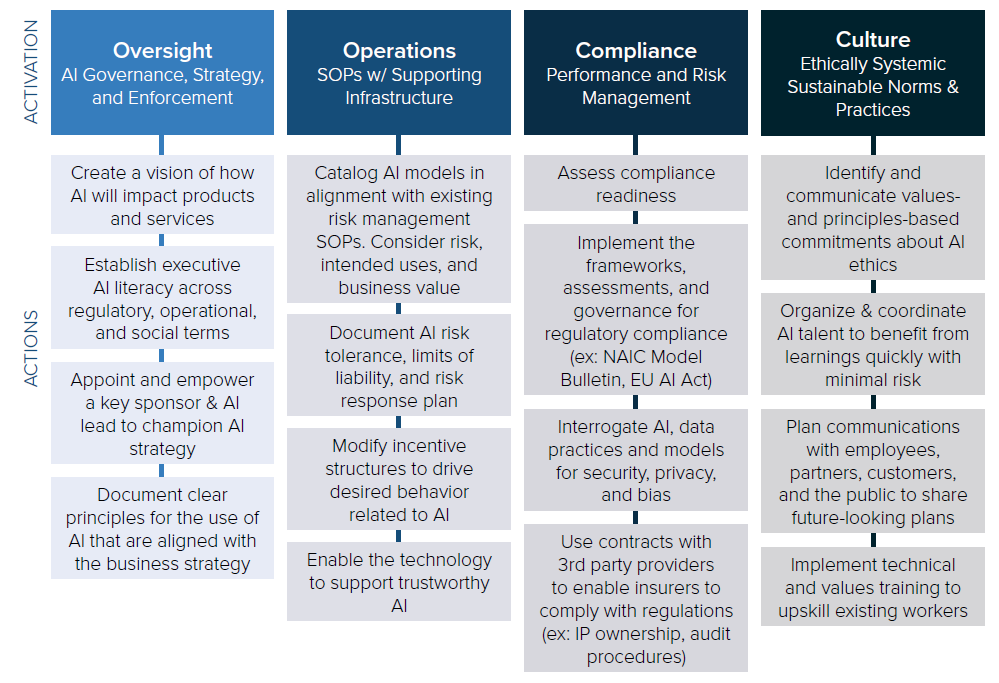

One such example involves PZU, the largest insurer in Poland. Recently, they concluded a board-level project to establish their AI identity leveraging SAS’ “Quad Approach.” The SAS AI Governance Advisory model addresses oversight, operations, compliance and culture.

After engaging with the SAS Data Ethics practice, PZU developed its unique AI framework, which in turn integrated with its strategy, technology and processes.

We see other leading examples of trustworthy AI adoption in the marketplace – such as Liberty Mutual’s Notice of Use of Artificial Intelligence US Consumer Bulletin and ERGO’s enterprise-wide use of Generative AI spanning 28,000 employees.

However, these frontrunners, by definition, represent the exception. Most insurers do not view technology as an enabler, have not built a principled approach to AI adoption and have not taken steps to upskill their workforce.

That said, our study did find the number one implementation priority for insurers is “support AI training and reskilling” (52%). This supports Boyd’s prior observation that the biggest opportunity for insurers lies in their greatest asset – their people.

AI requires governance and oversight

Make no mistake, insurers must use AI to stay competitive. In his recent blog, “AI is a 5-Layer Cake,” CEO of NVIDIA, Jensen Huang notes, “AI is becoming the foundational infrastructure of the modern world.”

I predict that by 2040, every insurer will be an AI company. Underwriters, adjusters and (sales) agents will work alongside AI in close collaboration. What will differ is that those same human employees will have the supervisory skill set to provide oversight to multi-agent tenants – similar to how front-line managers provide leadership to insurance teams today.

In this new reality, AI governance becomes non-negotiable; without it, you have no trust in AI systems.

In our most recent episode of Brewing Curiosity: Insurance Unfiltered, Brown puts this idea into perspective for the audience.

“What do we do about [the trust imbalance]? We make trust auditable.”

That means:

- A unified governance layer across underwriting, pricing and claims.

- Clear model documentation.

- Fairness and explainability tests as part of standard validation.

- Continuous monitoring after deployment. That is, not quarterly, not annually, but aligned to business volatility and drift.

Brown elaborates, “[We provide] AI literacy plus consistent controls, so trust becomes something we earn with evidence, not something we grant by default.”

I hope you join us on this journey as our video series continues. For now, stay curious, my friends!