About a year ago, I shared 5 predictions for fraud, AML compliance and security highlighting what we would likely experience in 2020. In this post, I’d like to take a quick look back at 2020 to review my predictions against what actually happened.

Clearly, COVID-19 had a major impact on all of us in 2020 – our personal lives, the companies we work for, and the economic and geopolitical environments. This in turn affected the predictions made at the end of 2019. Some expectations were solidified, while others were delayed. Despite what 2020 threw at us, three of last year’s predictions rang true, while partial progress was made toward the remaining two. All things considered, I’ll take the 80% hit rate and look for improvement in my predictions for 2021!

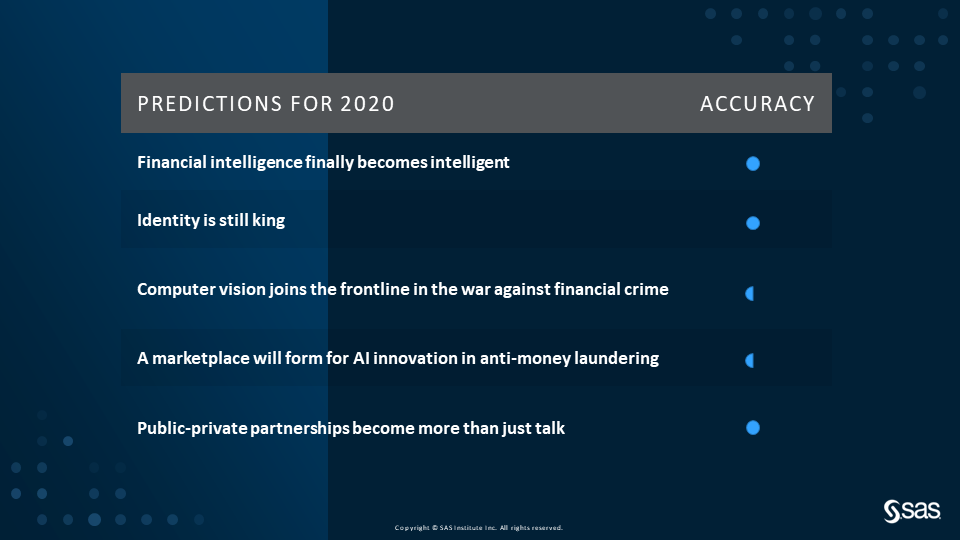

Let’s take a closer look to see how each prediction panned out.

Prediction 1: Financial intelligence finally becomes intelligent

“Financial intelligence will finally become a reality as multiple information sources unite and analytics connects the dots at scale – forming true, all-source-intelligence platforms.”

2020 prediction accuracy rating: 100%

There are numerous examples of this prediction ringing true based on advancements in supporting technologies. Of course, this is a journey that will continue in earnest for years to come. Below are a few supporting points from the 2020 report from the National Crime Agency, the UK’s Financial Intelligence Unit:

- Money denied to criminals was up 31% year over year as the number of suspicious activity reports (SARs) processed increased. This report highlights how data sharing via SARs adds value to law enforcement and civilian agencies.

- HMRC obtained £56m (more than $76 million) by matching SARs with other data sets for criminal and civil intervention.

- Egmont Group formed the Information Exchange Working Group across the public and private sectors to share information related to child exploitation.

There are also examples of transformation in payments that are hitting stride that streamline cross-border and cross-organizational data sharing. For example, P27 is a newly formed organization aiming to build the first real-time, cross-border payment system in multiple currencies. More efficient payments are crucial for economies as well as fostering innovation. With that as a foundation, we should not underestimate the value from integrated data and its use in detecting international crime.

Though not directly tied to financial intelligence, another example of connecting the dots at scale is contact tracing. (Consider this Oklahoma State University story.) Sophisticated algorithms have been deployed not only to link data, but to identify the significance of a contact and predict risk of infection. It’s amazing what we can accomplish in a short timeframe when we are all collaborating to solve a problem.

Prediction 2: Identity is still king

“Synthetic identity fraud will lead the way in the continued rise of identity fraud. That will require organizations to incorporate data from a wider range of third-party providers to combat fraud in this digital-first world.”

2020 prediction accuracy rating: 100%

This was the prediction most greatly solidified by the pandemic, as the way we transact has been forever changed. Many financial institutions are now seeing digital transactions in numbers they didn’t expect until 2025. Combined with government programs focused on getting funds in citizens’ hands as quickly as possible (e.g., Personal Paycheck Protection (PPP) and unemployment insurance disbursements), the environment in 2020 was ripe for identity theft and synthetics to wreak havoc on lending and payments.

Organizations from banks, to alternative lenders, to government agencies, to insurance companies relied on a wide range of data sources to verify identity. Data came from device reputation, biometrics, geo-location, telephony records and public record data – in amounts greater than ever before. Though we will not see final 2020 numbers reported for some time, there are a few intriguing statistics we can see now:

- From January to mid-July 2020, US consumers reported losing a total of more than $90 million to COVID-19-related fraud.

- While businesses are highly confident in their ability to stop fraud, so far 57% have experienced rising year-on-year fraud losses. This was often the result of an inability to authenticate customers.

- 85% to 95% of applicants identified as potential synthetic identities are not flagged by traditional fraud models.

Prediction 3: Computer vision joins the frontline in the war against financial crime

“Computer vision is primed to join the frontline in the war against fraud and organized crime by using analytics to turn images into intelligence.”

2020 prediction accuracy rating: 50%

As budgets shifted to address the impacts from the pandemic, programs focused on deployment of computer vision slowed in comparison to expectations. This resulted in delays in the full realization of this prediction. Innovative research and acceleration in some industries continued.

The insurance industry has used computer vision for several years in areas including validation of property & casualty claims (e.g., auto collisions, hail damage). The industry is accelerating usage for broader risk assessment, loss prevention, risk management and product innovation.

As health and economic environments improve, we will see computer vision deployed more widely for combating financial crime – whether in our ports, our borders or our physical ATM and digital transactions.

Prediction 4: A marketplace will form for AI innovation in anti-money laundering

“On the heels of the US regulatory joint statement on Innovative Efforts to Combat Money Laundering and Terrorist Financing, I predict that a marketplace for AI innovation will form.”

2020 prediction accuracy rating: 50%

Despite the challenges from remote interactions, I was happy to see sharing of information and methodologies from AI-based approaches to transaction monitoring in 2020. With conference attendance at all-time highs due to remote access, a platform existed for accelerated knowledge sharing – in levels of detail we hadn’t seen to date.

Collaboration between financial institutions and their regulators continued in earnest, as seen by production deployments of AI-based monitoring. The progress being made within trade finance around trade-based money laundering is a great example. The Financial Action Task Force calls this activity “one of the primary means that criminal organizations use to launder illicit proceeds.”

Global banks are now deploying ensemble machine learning models in production to automate what were typically hundreds of manual checks of trade transactions. These models, which score a combination of money laundering and fraud risks based on a wide swath of features, are seeing accuracy rates around 90%. This high accuracy allows redeployment of specialized resources to focus on high-risk relationships.

All that said, I still grade this prediction as partially correct – because the pandemic focused anti-money laundering innovation on operational effectiveness to control costs versus better alerting and risk management. Based on a new global ACAMS survey of AML professionals (full results to be released soon), 43% of organizations still have no imminent plans to deploy AI for financial crimes compliance. Many respondents have focused to date on robotic process automation, but don’t consider that “AI.”

Despite positive signs of collaboration, sharing did not occur at expected levels (in or outside of a formal marketplace). I am still convinced a marketplace for innovation sharing will form in the near future.

Prediction 5: Public-private partnerships become more than just talk

“2020 is the year when AI and machine learning will pave the way to better data sharing across organizations and industries.”

2020 prediction accuracy rating: 100%

Among the many examples of partnerships globally, the most recent guidance to 314B (Fact Sheet in December 2020) was the icing on the cake for this prediction coming true. The expansion of safe harbor – for sharing information where a financial institution has a “reasonable basis to believe the information shared is related to activities that may involve money laundering or terrorist financing” – greatly increases the opportunity to share data and subsequently apply analytics. Further, the guidance clarifies additional organizations that can participate in data sharing.

Formal programs, such as the FinCEN Exchange and FinCEN Innovation Hours, have picked up steam in the virtual environment. The FinCEN Exchange is a partnership between law enforcement and financial institutions to more effectively prevent terrorism financing, organized crime, money laundering and other financial crimes. Innovation Hours provides FinTech, RegTech and financial institutions an opportunity to share innovative ideas or approaches.

I have been very fortunate to be part of one such public-private partnership initiated by The Knoble. Sponsored by The Global Fund to End Modern Slavery (GFEMS), The Knoble and its public and private partners have formed a network for cross-industry data sharing with a goal of protecting vulnerable populations who fall victim to human trafficking, child exploitation and elder abuse. We as financial crime fighters all live with a broader sense of purpose, and this is one example where AI and machine learning will be applied to make a bigger impact.

2021: What's next?

At the end of 2020, I again shared 5 predictions for fraud, AML compliance and security – this time highlighting what 2021 has in store. Over the next 12 months, we will feel the impacts of many forces. These range from changing administrations to continued stimulus, from accelerated digital transformation to workforce optimization initiatives, and from historically high unemployment rates to headwinds on consumer spending.

Watch a video of my detailed predictions at the link below – and buckle up for what will be an intense ride.

Listen to my 5 predictions for 2021