In a previous blog post, we discussed how generative AI (GenAI) is experiencing unprecedented popularity, with organizations across various industries eager to unlock its immense potential.

We also highlighted potential use cases organizations must identify to unlock GenAI's full potential with credit customer journeys. These can include using chatbots for sales and marketing or natural language processing (NLP) for data analysis.

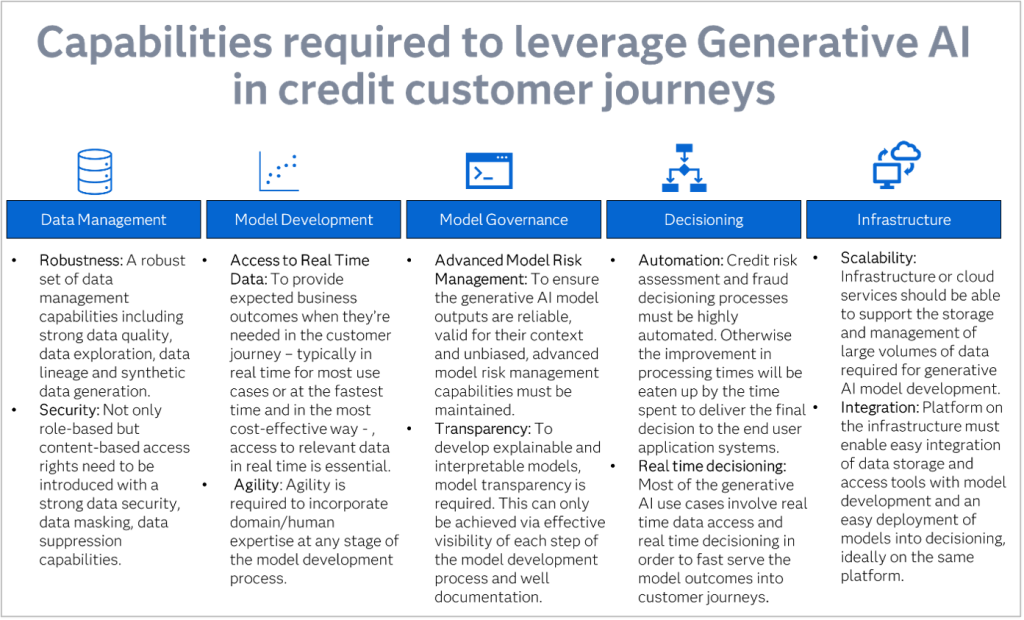

However, once the transformative use cases are identified, the second step is to validate whether the organization’s current technology can provide those capabilities. No matter what you're using GenAI for, this ensures robust data management, agile model development, stringent model governance, effective decision-making processes and scalable infrastructure.

The importance of data management

- Robust data management: To develop accurate outcomes and avoid ‘hallucinations,’ GenAI models need to be fed with a large amount of data, most of the time via isolated, internal and external data sources, both structured and unstructured. This requires robust data management capabilities, including solid data quality, data exploration, and seamless data connectivity, regardless of data location.

- Superior data security: GenAI makes it more critical to ensure the right people can access model development data. Role-based and content-based access rights, solid data security and masking and suppression capabilities must be introduced.

Developing agile models

- Access to real-time data: To provide expected business outcomes when needed in the customer journey, typically in real-time, access to relevant data in real-time is essential. This ensures timely and cost-effective decision-making.

- Agile model development: An agile model development technology is required to augment newly developed GenAI models with existing machine learning models. Agility is also necessary to incorporate domain/human expertise at any stage of the model development process, whenever required.

Avoiding risks with model governance

- Advanced model risk management: Given GenAI models' complexity, it’s harder to decide their general applicability and whether they underfit or overfit the data. To ensure GenAI model outputs are reliable, valid for their context and unbiased, advanced model risk management capabilities must be maintained.

- Transparency: Model transparency is required to develop explainable and interpretable models. This can only be achieved through adequate visibility of each model development step and thorough documentation.

Decisioning is also key

- Automation: To fully benefit from GenAI in credit customer journeys, credit risk assessment and fraud decision-making processes must be highly automated and integrated. Otherwise, the improvement in processing times will be eaten up by the time spent delivering the final decision to the user systems.

- Real-time decisioning: Real-time data access and leveraging GenAI models don’t enable the creation of successful customer credit journeys unless they’re supported with real-time decisioning to fast-track the model outcomes into customer journeys.

Checking on infrastructure and cloud services

- Scalability: Infrastructure or cloud services should be able to support maintaining the highest possible performance at the lowest cost for the storage and management of large volumes of data required for GenAI models.

- Integration: The platform on the infrastructure must enable easy integration of data storage and access tools with model development and easy deployment of models, ideally on the same platform.