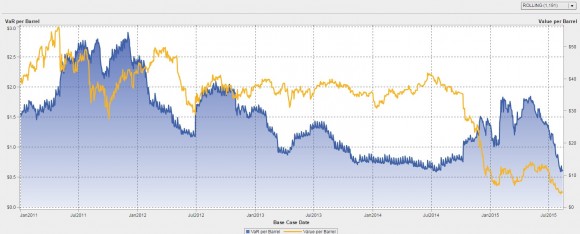

Since our last VirtualOil update in May, oil prices have continued to take a beating. As the chart of the rolling five-year portfolio shows, much of our strip of options is now out-of-the-money and the average value per barrel of that optionality has sunk below $7. No surprise then that our Value-at-Risk (VaR) has also dropped dramatically – at this point, we have very little left to lose.

If VirtualOil were an actual physical company, we would be repatriating our ex-pats, shutting down projects, cutting capital spending budgets and, eventually, facing layoffs and restructuring. But as a virtual company based on a stack of options, we can virtually shut-in while we ride out the devastating situation inflicted on us by the global crude oil markets. Our initial options costs are sunk, but the potential for our wells to become profitable again remains.

Even though we are underwater, our portfolio is still valuable because the market continues to offer the probability that our options will exercise in the money. That’s quantifiable: We can calculate precisely our potential to perform in the options market. But does that mean holding is the right business decision?

The forward curve has shifted down and become steeper, and the markets are telling us that we could be underwater for much of the rest of this year, and almost all of next. Today (August 27), the first forward contract for WTI over our strike price of $50 is Nov 2016. It might make better sense to consider selling all of our forward options now, cash out VirtualOil and restructure the portfolio at a lower strike price, back in the money, while retaining upside potential.

Where an actual company in our situation would likely exit the market, our virtual status allows us to be nimble. Should we get out of our unprofitable structure and reset the portfolio? We’ll take it to our virtual board – stay tuned for the answer in next month’s edition.

See below for additional visualizations of VaR back-testing and varying vintages.

Assumptions

The hypothetical derivatives-based oil production firm VirtualOil simulates the performance of a generic crude oil asset, and delivers sectorial exposure to the commodity oil market. Specifically, the VirtualOil structure starts up with an investment of $350MM in monthly average price call options with a strike price of $50 per barrel on the price of WTI light sweet crude oil. The strip of options starts at 10,000 barrels per day and extends out for 5 years with a 20 percent average annual decline in underlying notional barrels, replicating a physical oil asset. VirtualOil initially holds notional crude oil reserves of approx. 10MM barrels. Monthly cash flow is generated when the daily average WTI price relative to the preceding month exceeds $50 per barrel. Cash flow is reinvested monthly at 5 percent and the project winds up when the reserves are depleted.

VirtualOil is managed in SAS® BookRunner with reports surfaced in SAS® Visual Analytics. Learn more about SAS® BookRunner’s state-of-the-art Commodity Trading & Risk Management capabilities.

Disclaimer: This is a fictitious portfolio and is not a solicitation to trade.

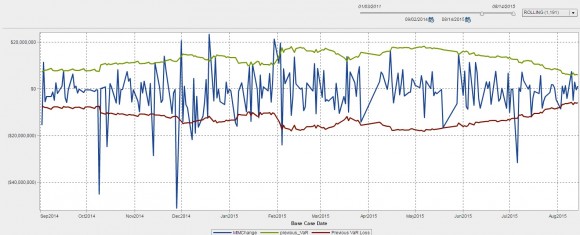

Chart: VaR Backtesting

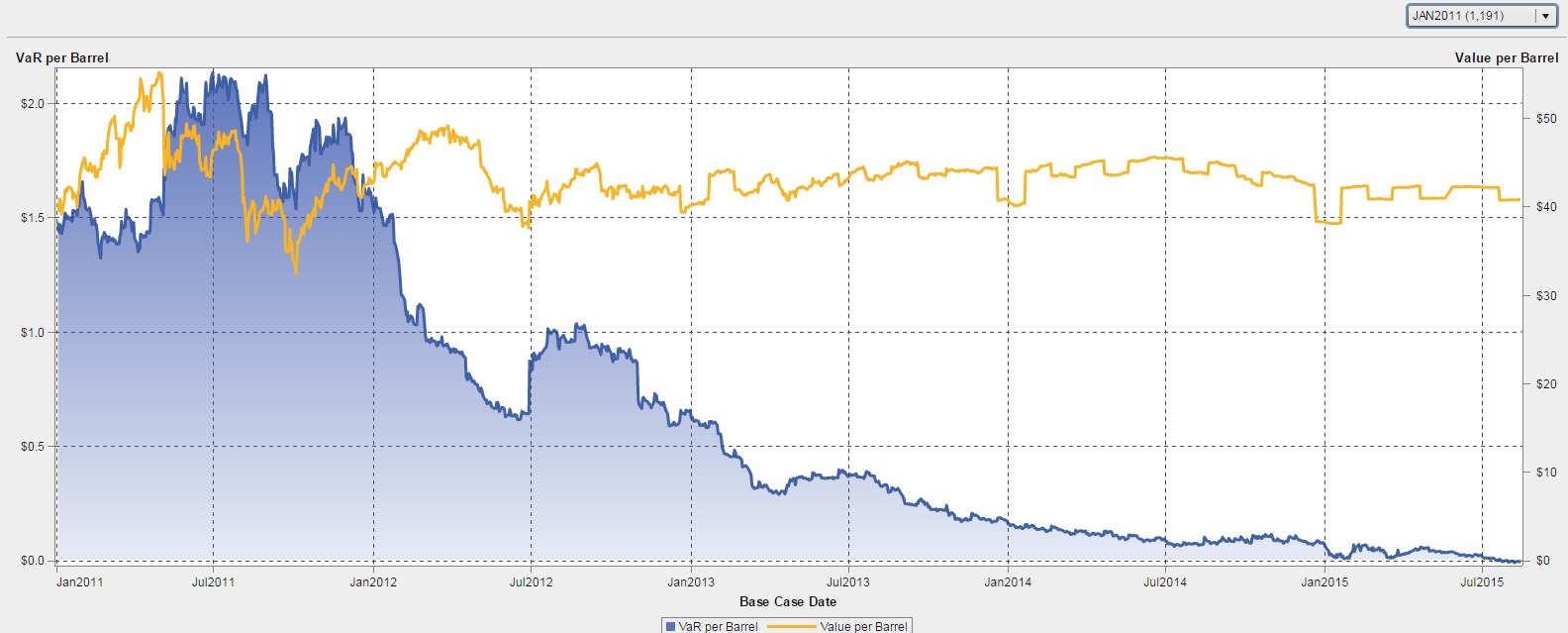

Chart: VirtualOil Jan 2011 Start Date Portfolio

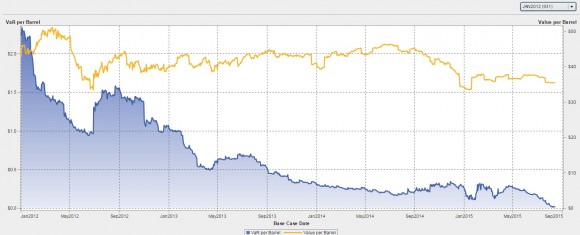

Chart: VirtualOil Jan 2012 Start Date Portfolio

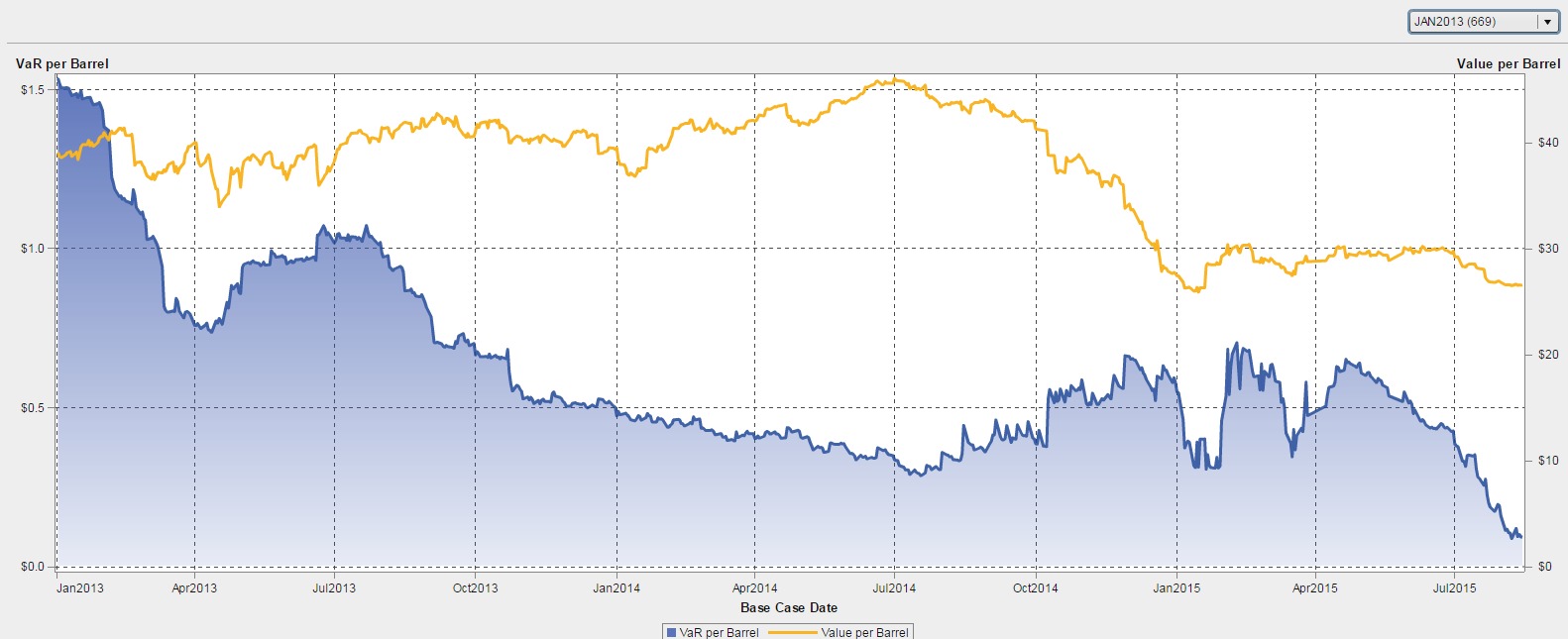

Chart: VirtualOil Jan 2013 Start Date Portfolio

Chart: VirtualOil Jan 2014 Start Date Portfolio