~ This article is co-authored by Binod Jha, Global Product Manager for Insurance Solutions at SAS, and Amol Kokane, Senior Development Manager for Insurance & Risk Management Solutions at SAS ~

How might insurance policies change if sensor data could be automatically transmitted and analyzed from your car, your home and even your clothes?

The Internet of Things (IoT) has the potential to transform both the business and the IT infrastructure of the insurance industry. The data captured and transmitted by multiple sensors and devices – each attached to an associated, insured risk – will redefine existing processes of underwriting and pricing.

Let's look at a few definitions before we get into the possible affects of IoT on the industry.

Insurance premium pricing is based on a set of rating parameters that are derived from predictive models built from historical loss data. The law of large numbers and the associated spread of risk exposures helps in arriving at the pure premium for a pool of homogenous risks. But it’s very difficult to calculate loss propensity at each risk and exposure level in this pool.

Underwriting and pricing happens when a policy is sold, but the risk (both in quality and behaviors) changes over time. This fact should be (but seldom is) factored in the underwriting on a regular basis. So while the insurance industry has historically been data intensive, its ability to monitor claim propensity at each risk and exposure level during the lifetime of the policy is limited. As such, premiums are subsidized by good risks, taking the same hit by association with the bad risks.

How does IoT change the game?

IoT makes it possible to capture rating parameters as well as the digital shadow (the historical data captured from devices and sensors) of insured objects and people, in real time. This huge amount of data can be analyzed for underwriting and pricing decisions at each exposure level, that is for each instance of the policy coverage period. This moves insurance to the realm of continuous calculations - thereby reducing incurred losses with proactive strategies vs. historical tactics. The IoT ecosystem has already matured enough to enable the early movers in this new IoT operating model for insurance.

What are the benefits of IoT?

For insurers, the benefits of analyzing IoT data include:

- Lower claim severity and frequency. Continuous monitoring of insured risks, real time prediction of loss propensity, and reliable loss control mechanisms will impact claim severity and frequency.

- More accurate risk assessment. Huge amount of granular data generated by sensors and devices attached to insured risks improves risk assessment accuracy and thus the underwriting process. In turn, this also reduces the suppression of material facts related to risk by customers at the time of policy acquisition.

- Improved claim servicing. IoT enables automated loss notification in case of an accident or hazardous situation. The details related to loss or damage are captured by sensors and devices. Claim processing cycle time and loss adjustment expenses will be reduced as a result.

- Higher customer satisfaction. Real time monitoring of insured risks and dynamic pricing creates transparency to both the underwriting and rating process. Educating customers on the factors that impact their specific insurance premium not only takes the required precautions needed to avoid premium loading, but also puts customers in more control of their plan. And it’s expected that with policyholders in the premium driver’s seat, so to speak, they’d be more satisfied, happier customers.

The entire insurance value chain – underwriting, policy servicing, claims, actuarial, reinsurance and customer service – are all impacted, maybe even disrupted, by IoT. Let’s focus how this may play out for a few lines of business.

Life and health insurance

Life and health insurance is expected to see the biggest impacts from IoT for a couple of reasons. Risk quality changes with lifestyle events (marital status) as well as with demographics (like age and occupation) impacts the baseline underwriting of the policy. With IoT, however, continuous monitoring of risk quality becomes a reality. The underwriting and pricing of insurance premiums won’t be limited to the inception of the policy – but will change during the entire coverage period. In this new world, the insurance premiums will fluctuate just as with monthly utility bills.

And the days may not be too far off when IoT wearable devices capture significant measures, like heartbeat, temperature, blood sugar, exercise duration and report them to insurers. Or when clinical diagnoses are be made from non-invasive methods, like analysis of sweat or tears. Premiums might even be calculated on a daily basis, transparent to the end customers - encouraging healthier lifestyles perhaps and reducing premiums accordingly.

Auto insurance

The first round of business model disruption has already taken place in the automotive side of insurance with the popular adoption of usage-based insurance (UBI) over traditional pricing in countries like the US, Canada, UK, Italy, Germany, and others. With UBI, vehicles are fitted with sensors that monitor driver behavior, to keep track of when, where and how the vehicle is in motion. The insurance premium is primarily determined on the basis of driving behavior, rather than proxy variables like vehicle make, model, and year. Enhancements to claims processing will likely be the next major improvement area for auto insurance – with automated notifications from these same telematics sensors for accident occurrence or non-typical driver profiling, helping carriers pinpoint events like accidents or theft.

Property insurance

It’s expected that property insurance will see an increased adoption of IoT in this decade. Smart homes, offices, commercial buildings and industrial installations can be fitted with sensors and devices that generate real time data on hazards from overheating malfunctions to building material strength. Not only can any accidents or breakdowns be immediately recognized, but gradual deterioration can be monitored to avoid substantial damages - bringing insurers into proactive service for property customers.

Home, office and industrial equipment can all be remotely monitored for ongoing situational assessment. Any measured factor leading to malfunction or damage can trigger notifications to repair shops or manufacturers for prioritized service. Smarter carpets that detect falling incidents can notify medical assistance, reducing staged accidents and liability claims. The scope of pragmatic applications is just beginning to emerge.

Insurance analysis in IoT

For this next generation of insurance applications to be successful, analysis of the sensors and all other streaming data will be necessary – to understand existing conditions and to postulate future scenarios accurately. How will this work?

The stream of incoming data first should pass through an initial set of rules and algorithms devised for assessing the data, normalizing it as necessary and evaluating risk, continuously. The risk patterns are already defined to recognize when conditions are met in real-time. How? The pattern resides in the system as data is continuously streamed through – calculating the conditions to new events. When conditions are met, a reaction is triggered, sending the appropriate person or system the instructions to take the next action. For example, if vehicle monitoring indicates speeding based on location-based limits with frequent acceleration followed by sudden breakeage, an alert can be sent to the driver to reduce speed.

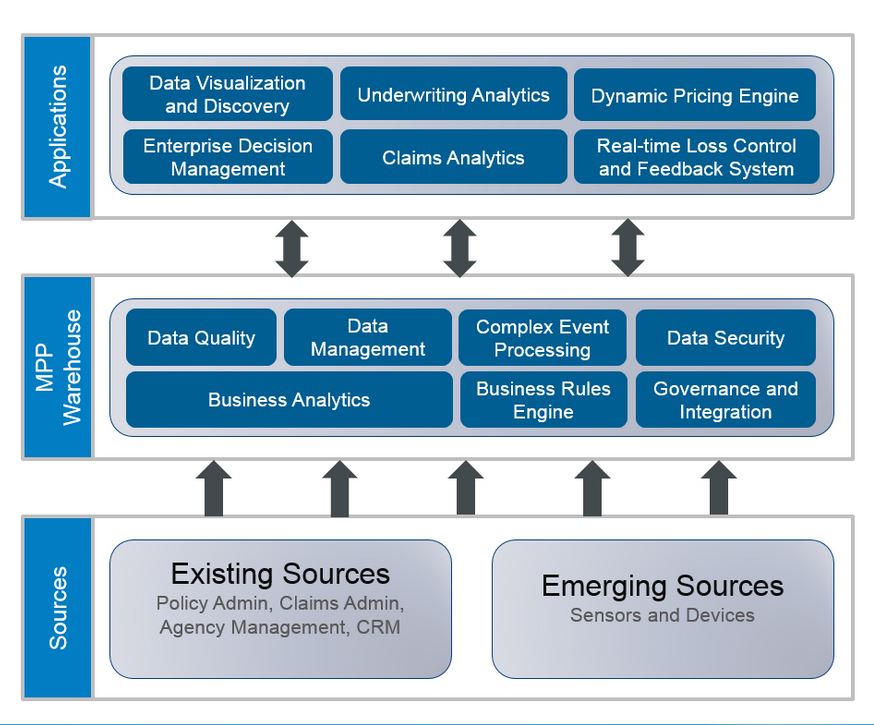

The high-volume and high-velocity granular data captured and transmitted from sensors and devices and attached to insured risks needs to be cleansed, organized and stored in a multi-parallel processing (MPP) data warehouse with effective history management. The stream of incoming data first should pass through an initial set of business rules and algorithms devised for continuous monitoring of risk. Any trigger of such rules should be able to send an appropriate feedback or control to the customer through state-of-the-art event stream processing system. The incremental data needs to be extracted from the warehouse and loaded into analytical input datasets for both modeling claim frequency and claim severity. The MPP environment supports high performance advanced predictive analytics and is used to discover any new significant rating parameter(s). The newly generated algorithm is then registered in a model management system and operationalized in the dynamic pricing engine.

Unlike the current industry adoption of analytics in limited parts of the business, this new, IoT driven, big data revolution will require mainstream adoption of analytics across the entire insurance value chain. Every part of the business will be supported by sophisticated algorithms – assessing the current risks and calculating the differential value. Insurance organizations will be on the forefront of technology adoption to invest in scalable and robust high performance platforms.

2 Comments

A good article. While you have covered the data aspects, organizations need to understand that "with new technology comes new thought" {aka the Aunt May quote from Spiderman}. The role of insurance companies are likely to change from policy management to customer risk management. Unless this change happens, it is highly unlikely for an insurer to institutionalize the IoT approach.

Refer an article I had written at http://crmzen.blogspot.in/2006/09/vision-to-have-vision.html

Binod & Amol - Excellent review of the predicted insurance industry evolution through IoT and analytics - both associated with long-overdue technology adoption. In monitoring this industry, I have looked forward to all lines of business equalizing through modernization. Impatient and demanding prospective / current policyholders and the increasing power and demands of insurer distribution channels are driving insurers to invest and catch up to their fellow vertical markets.

Though this evolution will be costly and adoption somewhat painful, Insurers will be so amazed at the new ways analytics will open profitability opportunities. Newly enabled, they will be advantaged in new product development and both risk & fraud mitigation, as well as enhancing policyholder & distributor experiences / satisfaction with a near / real time 360 degree information view - while continuously monitoring their business activities. Though the new age insurer must modernize to achieve these benefits, they will also sooner reap the associated value in doing so to be competitive.