The role of insurance is to bring some predictability, manageability and stability to a chaotic and uncertain world. In essence, it is a risk mitigation tool.

The role of the Chief Risk Officer (CRO) is to manage the overall risk strategy for the insurance company. They are responsible for defining the medium to long-term risk strategy for their insurance organization.

This strategy takes into consideration variables such as risk appetite, target market, customer segments, core products, distribution channels and expected return on investments. This is achieved by what is commonly referred to as the capital management and planning process.

The first step in the process requires insurers to identify and model all material risks that can potentially affect their solvency or the long-term value of equity. To have an efficient capital management framework, insurers also need to coordinate the actions of their risk units with their actuarial and finance departments. Planning and budgeting exercises that steer direction for operational actions should be coordinated with a view into risks, profitability and shareholder returns.

The second step is the necessity to align their decision-making process with estimates for how much capital the organization must have on hand in light of commitments and identified risks. This helps business line managers perceive the constraints and opportunities that economic capital presents in the areas of risk-based pricing, customer profitability analysis, customer segmentation and portfolio optimization.

With an effective capital management, insurers should be able to weather extreme internal risk events (e.g., a large operational risk event) and external scenarios (e.g., a catastrophic natural disaster) at an enterprise level. It also helps business line managers create favorable opportunities, as they can generate an optimized risk-return profile of their product portfolios.

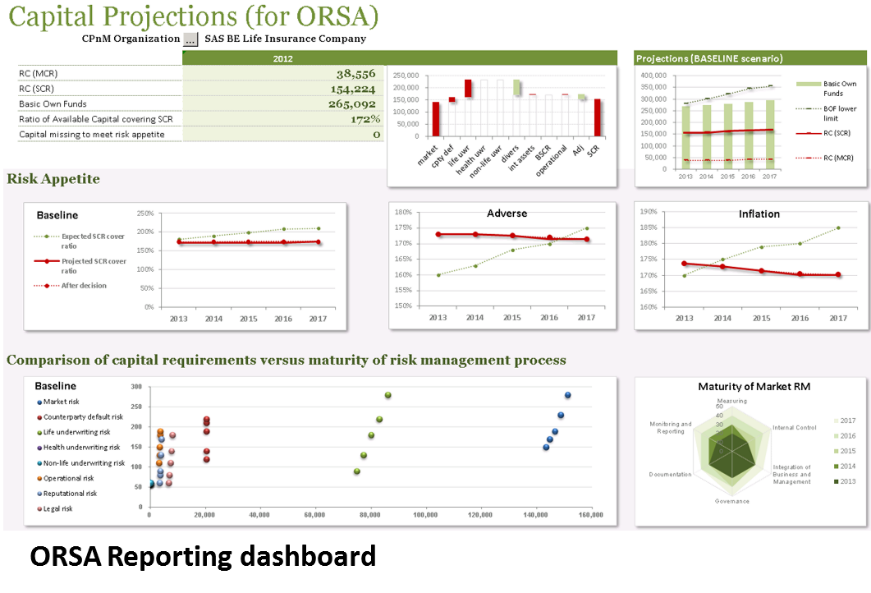

A new responsibility for many CROs is the emerging Own Risk Solvency Assessment (ORSA) that is required for Solvency II and other insurance regulations. One of the fundamental requirements of ORSA is that companies conduct an annual, forward-looking assessment. The goal is not only to demonstrate that the company’s current capital needs are appropriate, but also that its future capital needs will be met over a specified assessment time frame (usually three to five years). The report also allows regulators to get an enhanced view of an insurer’s ability to withstand financial stress.

A new responsibility for many CROs is the emerging Own Risk Solvency Assessment (ORSA) that is required for Solvency II and other insurance regulations. One of the fundamental requirements of ORSA is that companies conduct an annual, forward-looking assessment. The goal is not only to demonstrate that the company’s current capital needs are appropriate, but also that its future capital needs will be met over a specified assessment time frame (usually three to five years). The report also allows regulators to get an enhanced view of an insurer’s ability to withstand financial stress.

With the recently launched SAS Capital Planning and Management solution, CROs can perform the quantitative aspects of an ORSA, taking into account projected balance sheets, income statements and risk appetite with the capability for iterative scenario analysis and stress testing.

To learn more about emerging insurance regulations, download the white paper “ORSA: The New Kid in Town”.”

Insurance and risk have always gone together. However, as insurance becomes more complex and sophisticated, the rise of the CRO is inevitable. and the importance is undeniable.

I’m Stuart Rose, Global Insurance Marketing Director at SAS. For further discussions, connect with me on LinkedIn and Twitter.