As a marketer, one of the highlights of the SAS Financial Services Executive Summit has been the interactive session titled "Exploring and Exploiting Trends to Really Understand Today's Customer." The session involved all participants engaged in case studies, which included a facilitator and graphic artist from Matter Solutions.

This session provided the attendees with the ability to explore a common challenge we face as marketers - that our customers and their buying behaviors are moving targets, changing as quickly as the times. So how can we anticipate shifting market segments so we deliver relevant and timely products and services that meet their needs?

One important step we can take as marketers is to pay close attention to our assumptions, because in a world with so much uncertainty, it's important to know the difference between facts and assumptions in our models, and also whether the facts are accurate and that the assumptions are valid. It sounds like an academic exercise, but it is definitely rooted in everyday practicality because we all make assumptions whether we are conscious of them or not. One mentor in my early career once told me, "I pay you to manage, because if we had 100% of the data needed, then I wouldn't need to hire you. We're lucky if we have 60 - 70% of the information needed, so you have to fill in the missing 30 - 40%." In that case, of course, the 30 - 40% are the all-important assumptions.

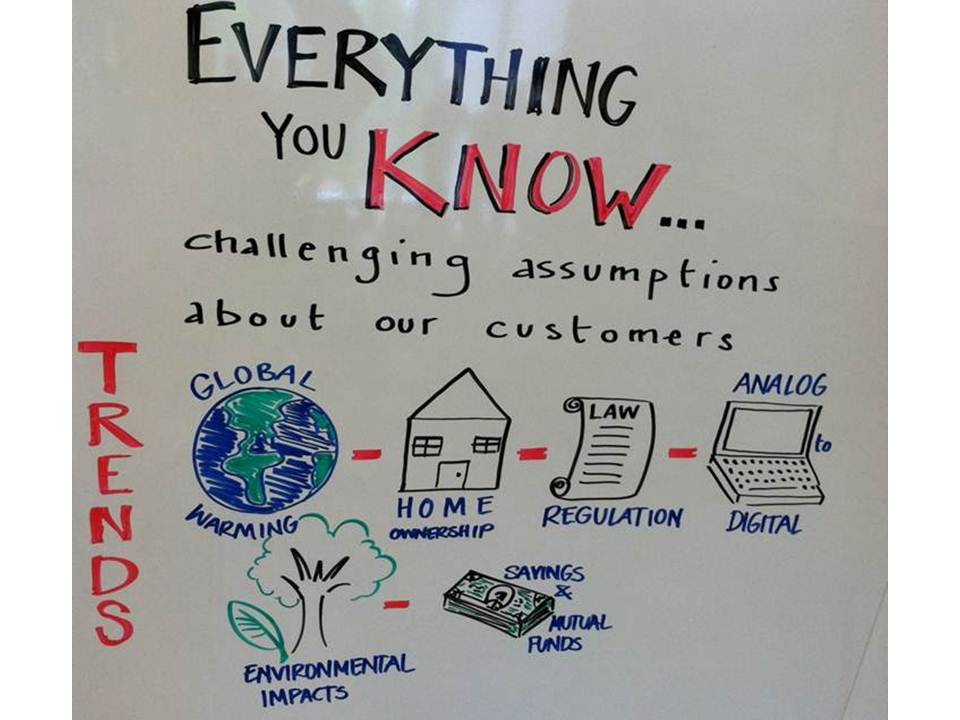

With a room full of banking and insurance executives, our facilitator gathered examples of assumptions that included factors such as home ownership rates, rational regulatory frameworks, stable energy prices / predictable natural resources, the shift from analog to digital communications, etc. For marketers, examples of assumptions include segmentation factors, accurate model scoring, open rates and click-throughs. And while we do our best to know what resonates with our audience, we even make assumptions about the relevance of the content we create.

Marketers are asked to paint a picture of the world our company operates in, so how can we do that when there is so much change going on? One approach to envision clusters in our data that form the segments we use to guide how we interact with our customers. There are usually outliers in our models, and then there are areas between the identifiable clusters, so the gaps between the outliers and the clusters are potential areas that can be arbitraged as you refine your model. Translated to the baseball world of Billy Beane, those are where the undervalued players are. It follows then that if you are re-segmenting frequently, then you are arbitraging the assumptions in your previous model.

As I absorbed the lessons of this session, I kept thinking how important it is for marketers to hone their skills in discovery and exploration. It's really all about critical thinking that has you asking the right questions and never taking anything for granted. I also think its about developing the right instincts for filtering out the noise from the signal, and that's certainly one place where customer analytics can help. Considering how much of the big data issue facing most organizations is customer data, and that some of the most important data are hidden in the vast tsunami of unstructured social media information, that's where social media analytics, customer experience analytics, marketing automation and other tools can empower the marketer to achieve some balance with empowered consumers.

Earlier in the day, Billy Beane gave an example of a bunt ball as a baseball tactic assumed to be good for getting on base. In Financial Services, a painful equivalent of the bunt ball is that subprime borrowers are fit to hold mortgages, built on the assumptions that home prices are ever-spiraling upward, and that people will always pay their mortgage even when financially strapped. The fallacy of those assumptions is well documented, including the latest reports showing that as many as 30% of borrowers, or 16 million homeowners, currently have negative equity.

Fortunately for marketers, not all the bunt ball equivalents facing them are as potentially catastrophic as the subprime mortgage crisis, but as we look to be sure we understand the customer, it behooves us all to check our assumptions.

Do you know what your bunt ball equivalents might be?